Europe drifts towards the brink of a cataclysm

Summary: This is a follow-up to The Fate of Europe, nearing the point of decision. That post discussed the objective factors — and the timing of events. Here we look at subjective but potentially decisive factors.

From the previous post — At some point Europe will decisively choose to either unify or break the European Monetary Union. Both options can work if done with determination and skill. Both have large costs. Neither Europe’s leaders or peoples yet know which path they will choose, so neither do we. Although most US experts believe they will choose to break the EMU in some fashion, the recent Berlin State elections showed surprising strength for the parties supporting unification. That should not surprise, as unification would give Europe powerful competitive advantages in the 21st century. Continued dithering guarantees disaster.

Contents

Background

Today’s Situation

Have people lost confidence in their leaders?

For more information

(1) Background

Norman Angell wrote The Great Illusion (1909) to show that a major war in Europe would benefit neither victors nor losers. Angell said that Europe’s nations were economically integrated to the point that war would prove too disruptive, so as to deter wars or end them quickly. Therefore, despite the arms race then underway, militarism was no longer useful for nations.

The book became a best-seller. But in 1914 Europe acted illogically (the result proved that they should have listened to Angell). Europe may do so again soon.

The cost of a disruptive crisis would be severe to every nation in today’s highly integrated Europe — no matter if the result is unification or divorce. This ominous near-certainty should force a highly coordinated, tightly planned response by both individual nations and Europe’s multilateral institutions (and the IMF, as the world will also suffer). Divorce or unify. Both work if done with determination and skill; both have large costs.

But there are a host of factors preventing a rational response. Fear of costs and potential disaster. Hatred between nations. Leaders’ delusional optimism (we can manage events, so there is not need to plan). And others.

(2) Today’s situation

“They have six weeks to resolve this crisis.”

— British finance minister George Osborne on 23 February 2011, referring to the G-20 meeting in Cannes on November 3 (source: Reuters)

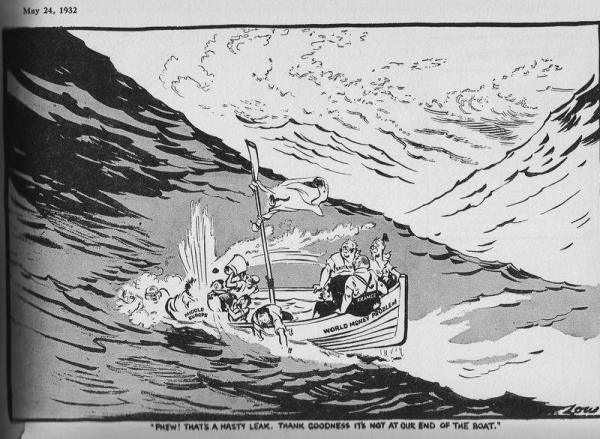

That’s a nasty leak. Thank God it’s not at our end of the boat!

Can Europe’s governments, on their own or through multinational institutions, act rapidly on sufficient scale? This, of course, was the problem in 1929. Even if they had seen the necessity, they probably could not have acted with the necessary speed and scale.

There are tools at hand, earnestly discussed today, to prevent a crisis.

A large fund (perhaps 3 trillion Euro) to stabilise the banks if Greece defaults

Using the European Financial Stability Facility (EFSF, now proposed to be 440 B euro) to leverage resources of the ECB

Using the EFSF to provide guarantees to buyers of sovereign or bank bonds

Implement the European Stability Mechanism (ESM) faster than planned, perhaps in early 2012

Force the ECB to cut rates and make massive purchases of sovereign and bank bonds

Even if fully implemented, these probably do little but buy time. The time expensively bought by previous programs has been squandered. None address the rot at the core of the European Union: lack of popular support for the project.

(3) Have people lost confidence in their leaders?

[…]

Internal political conflicts like this turn even the most skilled political engineers into:

We’re off to the next EU meeting!